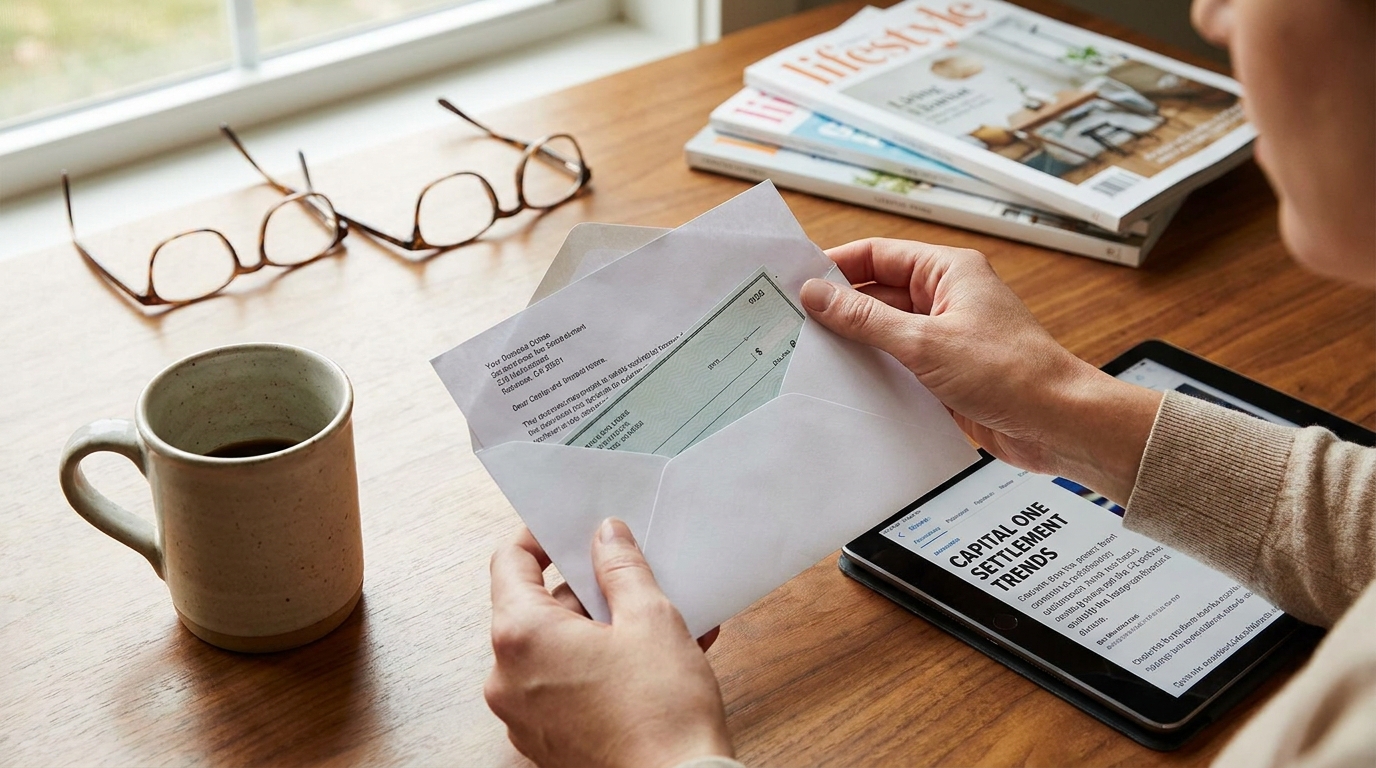

If you opened your mailbox lately and found an unexpected check from a Capital One settlement, you might be wondering if it is even real. It is actually part of a massive effort to make things right after years of legal battles. Between the 2019 data breach that hit 98 million people and the more recent Capital One $425 million settlement over interest rates, there is a lot of money and confusion moving around right now.

It is easy to get these cases mixed up, especially since a second wave of payments just went out in September 2024. While the window for a Capital One data breach claim closed for most people back in 2022, you might still have valuable perks you did not even know about. Staying on top of this matters because some of these benefits, like identity restoration and insurance, are active for years to come.

This guide will show you how to check your payment status and what to do if your check expired before you could cash it. We will also look at the security features available through 2028 so you can get every bit of value from these settlements.

Did you find a surprise check from Capital One in your mail recently? You aren't alone. There is a lot of confusion right now because two different settlements are overlapping. While the 2019 data breach affected 98 million people, a newer $425 million settlement involves interest rates on 360 Savings Accounts. If you saw a payment arrive around September 4, 2024, that was likely a second-round distribution for people who already filed claims.

But what if you missed the original deadlines? While the window for cash claims for lost time closed in 2022, you still have active benefits. Capital One extended their Identity Defense and Restoration Services through February 13, 2028. This includes dark web monitoring and a $1 million insurance policy for identity theft. Even if the cash window is mostly shut, that long-term protection is still on the table for you to use right now.

Key insights:

- Cash claim deadlines for the 2019 breach have passed, but identity protection services are active until 2028.

- The September 2024 payments are a second-round distribution for people who already had approved claims.

The $425 Million Interest Rate Settlement Explained

Have you ever looked at your bank statement and wondered why your high-yield interest rate felt a bit stagnant? That specific frustration is at the heart of a massive $425 million settlement involving Capital One. This isn't about a tech glitch or the 2019 data breach that hit 98 million people; it's about how the bank managed its 360 Savings accounts over several years. The litigation argued that Capital One essentially left long-time customers in the dust while offering much better deals to new sign-ups under a slightly different account name.

To qualify as a class member for this specific payout, you generally needed to have a Capital One 360 Savings account during the period when the bank was allegedly suppressing rates for legacy holders. The settlement reached such a staggering number because of the sheer volume of customers involved and the length of time their money sat in accounts earning less than it should have. It serves as a loud wake-up call for the banking industry about transparency. Think of it as a penalty for the gap between what customers expected and what they actually received.

The core of the legal fight was the difference between 360 Savings and the newer 360 Performance Savings options. While the names were nearly identical, the interest rates were worlds apart. Capital One allegedly kept the original 360 Savings accounts at a lower rate while marketing the Performance version with the high yields you see in commercials. Most people saw the 360 branding and assumed they were getting the best deal available. In reality, their money was parked in an account that was no longer competitive.

What does this mean for your current banking habits? It is a reminder that set it and forget it might be costing you real cash. If you haven't checked your specific account name and compared it to the bank's current top-tier offerings lately, you might be stuck in a legacy tier. Banks often launch new products to attract new capital, leaving older accounts to stay behind with lower returns. This settlement proves that those small percentage points add up to hundreds of millions of dollars over time.

While the window for many monetary claims in the separate data breach settlement closed back in 2022, this interest rate litigation focuses on a completely different kind of loss. It is about the loss of potential growth. It's also a good time to remember that even if you missed out on the cash payouts, some benefits like identity restoration services are still active through 2028. Staying informed is the only way to make sure you aren't leaving money on the table.

Key insights:

- The $425 million settlement specifically addresses interest rate discrepancies rather than the 2019 data breach.

- Legacy 360 Savings accounts were often kept at lower rates while newer Performance accounts received higher yields.

- Class members include customers who held these legacy accounts while the bank marketed newer, higher-paying versions.

- Checking your specific account name is vital because similar-sounding bank products can have vastly different interest rates.

Was Your Interest Rate Artificially Low?

Did you open a savings account years ago thinking your money was earning top-tier interest? Much like a cat finding a sunny spot that eventually moves, you might be surprised to find your balance left in the shade. A $425 million settlement recently addressed claims that Capital One left legacy 360 Savings customers stuck with lower rates while offering better deals to newer accounts.

The lawsuit argued that the bank was not transparent about 360 Savings no longer being their best product. This created a two-tier system where loyal customers earned less than new 360 Performance Savings holders. It is a frustrating reality showing how legacy labels can be a trap for your cash, much like a cardboard box that looks comfy but is actually too small.

What does this mean for you? Banking is not a set it and forget it deal. Even if you missed specific claim deadlines, you should check your interest rate today. Banks often launch new products with better perks while letting old ones wither. If your rate is low, pounce on a modern account that actually keeps pace with the market.

Key insights:

- The 425 million dollar settlement highlights a significant gap between legacy 360 Savings and newer Performance Savings rates.

- Loyalty does not always pay in banking; legacy accounts often stay on lower interest tiers unless you manually move your money.

- Checking your current APY is essential because banks rarely automatically upgrade older accounts to their highest-paying products.

The 2019 Data Breach: Why the Story Isn't Over

Remember the 2019 Capital One data breach? It was a massive story at the time, affecting about 98 million people in the U.S. alone. But if you think that chapter is closed, think again. The legal fallout has been long and complicated, involving not just the breach itself but also a separate 425 million dollar settlement over 360 Savings Account interest rates. For most people, the data breach settlement isn't just a one-time check you cashed and forgot about. It was designed to provide a safety net that stretches nearly a decade into the future. This matters because identity theft doesn't always happen the moment your data is stolen. Sometimes, hackers sit on information for years before using it, which is why the benefits were built to last until 2028.

The 2028 extension for identity protection is probably the most significant part of the story that people miss. Originally, these services weren't supposed to last this long. But the settlement was updated to ensure that class members have five full years of protection, which is two years longer than the original plan. This isn't just about peace of mind; it's a practical response to how modern cybercrime works. By keeping these services active through February 13, 2028, the settlement provides a buffer during a window when your leaked information is still likely to be floating around the darker corners of the web. It's a rare instance where a legal agreement actually looks ahead at the long-term reality of digital risk.

Now, let's talk about the money. You might have been surprised to find a check from the settlement administrator in your mailbox around September 4, 2024. This was a second wave of payments sent out to people who were already eligible. Why now? Often, these extra payments happen because there is money left over in the settlement fund from uncashed checks or administrative adjustments. If you found one of these checks but it is already past its void date, don't just toss it in the bin. You can actually request a reissue. You will need to get in touch with the settlement administrator through the official website. They handle these requests regularly, so it is a fairly straightforward process to get your payment updated and back in the mail.

Beyond the checks, there is a benefit you might have completely overlooked: Identity Defense Services. This is much more than a simple credit alert. It includes active dark web monitoring for your Social Security number, date of birth, and even your passport number. If your info pops up where it shouldn't, you get an alert immediately. Perhaps the biggest perk is the 1 million dollar insurance policy that comes with the membership. This policy has no deductible and covers the costs associated with restoring your identity if the worst happens. You also get access to security freezes across various categories, from credit bureaus like Experian to specialty finance and even utility databases. If you haven't activated these services yet, it is worth doing now because they stay active for several more years.

If you ever run into trouble, the settlement also provides Restoration Services. This means you aren't just left to figure things out on your own with a DIY guide. You get access to U.S.-based fraud resolution specialists who can help you place fraud alerts, dispute wrong information on your credit report, and even work with law enforcement if needed. While the deadline to file a new claim for lost time or out-of-pocket expenses passed back in September 2022, these defense and restoration services are the only active benefits still available. They are essentially a pre-paid insurance plan for your digital life, and since you're already part of the class, there is no reason not to use them.

Key insights:

- Monetary claims are officially closed, but identity protection benefits remain active until February 2028.

- A second round of settlement checks was distributed on September 4, 2024, to eligible class members.

- The identity theft insurance policy provides 1 million dollars in coverage with no deductible for recovery costs.

- Settlement members can request a check reissue if they received a payment that has since expired.

The Second Wave of Payments in 2024

Did you find a surprise in your mailbox lately? On September 4, 2024, Capital One sent out a fresh wave of checks to eligible claimants. This happened because there was still money sitting in the settlement fund from the 2019 breach and interest rate litigation. When people forget to cash their first checks, that extra cash gets rounded up and redistributed to the rest of the group. It is like a small, unexpected win for your bank account.

But what if you found your check under a pile of mail and it is already expired? Don't worry just yet. You can usually ask for a reissue by contacting the settlement administrator. They are the ones managing the $425 million litigation funds. Just reach out through the official settlement website to explain the situation, and they can often send a new, valid check your way.

This second round is a clear sign that this years-long legal saga is finally winding down. Even though the window to file new claims closed back in 2022, these payments make sure the money actually gets into the hands of the people it was meant for. If you got one, make sure to head to the bank quickly so it does not turn into a useless scrap of paper.

Key insights:

- The September 2024 payments are a redistribution of unclaimed settlement funds.

- Expired checks can often be replaced by contacting the settlement administrator directly.

- While new claims are no longer accepted, existing members are still seeing the final payout stages.

Identity Defense: The Benefit You Probably Forgot You Had

While everyone is checking their mail for a settlement check, you might be sitting on a much more valuable perk without even knowing it. The Capital One data breach settlement did more than just hand out cash. It provided a security layer that many people have not used yet. Even though the deadline for money claims passed in 2022, your identity defense services were extended. You are actually covered until February 13, 2028.

This service is much more than a basic credit ping. It scans the dark web for your most sensitive information, like your social security number and passport details. If someone tries to use your data, you get an alert immediately. The best part is the insurance policy. You get up to $1 million in coverage for identity theft costs with no deductible. If things go wrong, U.S. based fraud specialists are there to help you fix the mess and coordinate with law enforcement.

If you have not turned these features on yet, do it now. Think of it as a free safety net that stays active for years. It even covers you for lost wallet protection and various security freezes. It is a rare case where the extra benefits might be worth more than the actual cash. Check the settlement site to see your status and get protected before you forget about it again.

Key insights:

- Identity protection benefits remain active until February 2028 even though cash claim windows have closed.

- The settlement includes a $1 million insurance policy with no deductible for identity theft recovery.

- Dark web monitoring covers high-risk data like passport numbers and social security numbers.

Getting the Most Out of the Settlement Security Features

When people hear about a settlement, they usually look for a check in the mail. While a second round of payments went out in September 2024, the real win is the long term security help. If you were one of the 98 million people caught up in the 2019 breach, you actually have protection until early 2028. The restoration services are the standout feature here because they offer something money cannot buy: time and peace of mind.

Think of these services as a professional team in your corner. Instead of just getting a notification that something is wrong, you get access to U.S. based fraud specialists. These experts handle the hard parts, like talking to law enforcement or arguing with creditors who claim you owe money you never spent. It is a huge step up from a standard fraud alert. While the window to claim lost time or cash ended in 2022, these active benefits are still there for you to use if things go sideways.

One of the best moves you can make is using the security freeze feature. Most of us stop after freezing our files with the big three credit bureaus. But that is only half the battle. To really lock things down, you need to look at agencies like Innovis and Sage Stream. These specialty bureaus track things like your utility bills and smaller loans. The settlement makes this process much simpler for class members.

By freezing your data across all these categories, you are making it much harder for someone to use your name for a new phone plan or a quick loan. It goes beyond just credit scores and looks at your financial life as a whole. It might feel like a lot of steps, but having that wall up is the best way to stay safe until the coverage ends in 2028. The goal is to be proactive now so you do not have to be reactive later.

Key insights:

- Restoration services provide direct help from U.S. specialists until February 2028.

- A security freeze should include specialty bureaus like Innovis and Sage Stream to be effective.

- Security benefits remain active even though the deadline for monetary claims has passed.

The Power of the Security Freeze

Most people think freezing credit with the 'Big Three' bureaus is enough. It isn't. While Experian, Equifax, and TransUnion are the big names, smaller players like Innovis and Sage Stream also hold your data. These specialty agencies often fly under the radar, but they are exactly where identity thieves look when the main doors are locked.

Since the 2019 Capital One breach exposed nearly 98 million people, the settlement has made securing your information much simpler. You have access to Identity Defense Services through February 13, 2028. This includes help setting up freezes across several categories, from credit to specialty finance and even utility records.

Think of it as a full-house lockdown instead of just locking the front door. Because the settlement provides restoration specialists, you don't have to deal with these niche agencies alone. If you were part of the class, these tools ensure your financial life stays private long after the settlement checks have been mailed.

Key insights:

- A security freeze should extend to specialty agencies like Innovis and Sage Stream, not just the major bureaus.

- Settlement benefits like Identity Defense are active until 2028, offering professional help to secure your data.

Did You Miss the Deadline? What to Do Now

If you just found out about the Capital One settlement and realized the September 30, 2022, deadline for cash claims is long gone, you might feel like you have missed the boat entirely. It is frustrating to hear about people getting a second round of checks in late 2024 while your wallet stays empty. But do not click away just yet. While the window for claiming money for lost time or out-of-pocket expenses is shut tight, there is still a safety net available for many of the 98 million people affected by that 2019 cyberattack.

Here is the thing: the settlement was about more than just cutting checks. It also included long-term protection that actually lasts for years. If you are part of the settlement class, you can still access Identity Defense and Restoration Services through February 13, 2028. This is a big deal because it provides a full five years of protection, which is two years longer than the court originally planned. If your data was part of the breach, these services are currently your most valuable active benefit.

What if you suspect your data was recently compromised? You do not need to have filed a claim back in 2022 to use the restoration features. You can get help from fraud resolution specialists who assist with disputing inaccurate information or setting up security freezes across credit and utility accounts. Think of it as a professional team in your corner until 2028. So, while the cash might be off the table, the protection definitely is not.

Key insights:

- Monetary claims for the 2019 breach officially closed on September 30, 2022.

- Identity Defense and Restoration Services remain active for eligible members through February 13, 2028.

- Restoration services include access to U.S.-based fraud specialists and help with security freezes across multiple financial categories.

Frequently Asked Questions

How do I know if I'm part of the Capital One settlement?

You are likely part of a settlement if you were one of the 98 million people affected by the 2019 data breach or if you had a 360 Savings Account during the interest rate dispute. Usually, the settlement administrator sends out an email or a letter to let you know if you are eligible based on their records.

It is important to remember that there are actually two different legal situations. One is the older data breach case and the other is a newer 425 million dollar settlement about savings account interest rates. If you had an account during those specific times, you probably qualify for the benefits tied to those cases.

If you are not sure, you can search your inbox for messages from the official settlement administrator. Just be careful to only use the official websites mentioned in those notices to avoid any scams.

Can I still file a claim for the Capital One data breach in 2024?

No, the window to file a new claim for cash or lost time ended on September 30, 2022. If you did not get your claim in by that date, you cannot start a new one for money now.

But here is the thing that many people miss. Even though you cannot ask for a check anymore, the identity protection benefits were extended for a long time. If you are already a member of the settlement, you still have access to identity defense and restoration services through February 13, 2028. This includes things like dark web monitoring and help from fraud specialists if someone steals your identity.

Also, if you already filed a claim and were approved, keep checking your mail. A second round of payments was actually sent out in September 2024 for people who had valid claims and were waiting for their share.

Why did I receive a second check from the Capital One settlement?

You likely received that second check because the settlement administrators issued a new round of payments on September 4, 2024. This happens when there is money left over in the fund, often from people who never cashed their first checks or from interest that built up while the case was being settled.

Instead of the money sitting there, they split it up among everyone who filed a valid claim the first time around. It is basically a bonus payment for people who already qualified. Just make sure you get it to the bank quickly because these checks usually have a pretty short window before they expire.

What is the difference between the $425 million settlement and the data breach settlement?

It is easy to get these confused, but they are actually two different legal battles. The 425 million dollar settlement is specifically about interest rates for 360 Savings Accounts. On the other hand, the data breach settlement is about the 2019 cyberattack that exposed personal info for about 98 million people.

The data breach case is much older and its main window for filing money claims closed back in late 2022. However, that settlement still offers identity protection and restoration services until early 2028. The interest rate case is its own separate thing with different rules for who gets paid and why.

Conclusion

So where does this leave you? Between the interest rate payouts and the data breach fallout, there is a lot to track, but the big picture is clear. These settlements are not just about a single check. They are about holding big banks accountable and giving you the tools to keep your financial life secure for years to come.

If you missed the early deadlines for cash, remember that the security features are still yours to use until 2028. Your best bet right now is to double-check your mail for any 2024 reissue checks and activate that identity monitoring if you have not already. It is a free layer of defense that is too good to ignore.

The checks might eventually stop arriving, but your focus on security should not. Take the win, use the tools provided, and stay in the driver's seat of your own data. It is the best way to make sure a past breach does not become a future problem.